Meaning Of Book Profit For Mat Computation

Book Profit Definition Examples How To Calculate Book Profit

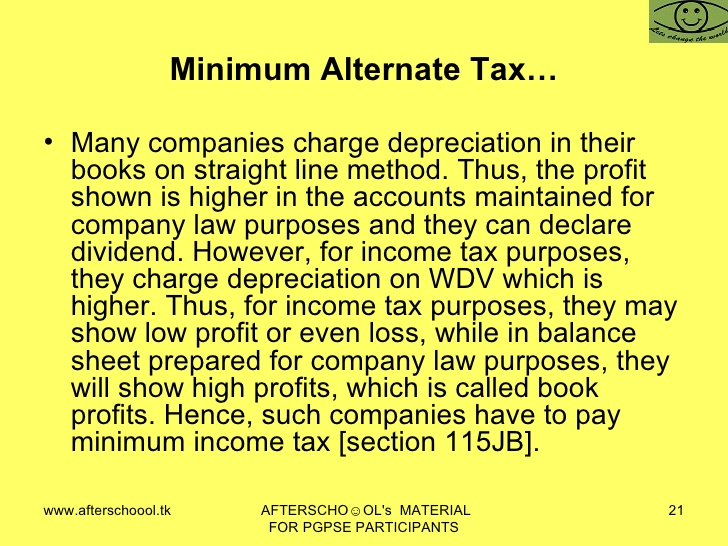

Minimum Alternate Tax

Minimum Alternate Tax Mat U S 115jb Of Income Tax Act 1961 V V Reddy Associates

Minimum Alternate Tax And Alternate Minimum Tax 115jb And 115jc

Minimum Alternate Tax Section 115jb How To Compute Arthikdisha

Ind As And Mat Provisions Sec 115 Jb Of Income Tax Act

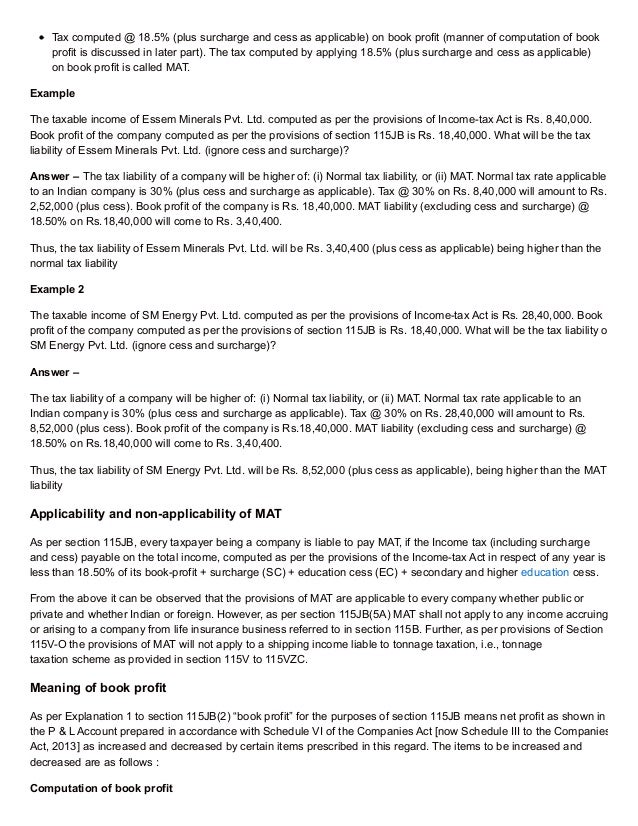

Minimum alternate tax mat.

Meaning of book profit for mat computation.

Cbdt Circular Of Clarifications Faqs On Computation Of S 115jb Book Profit For Ind As Useful Miscellania

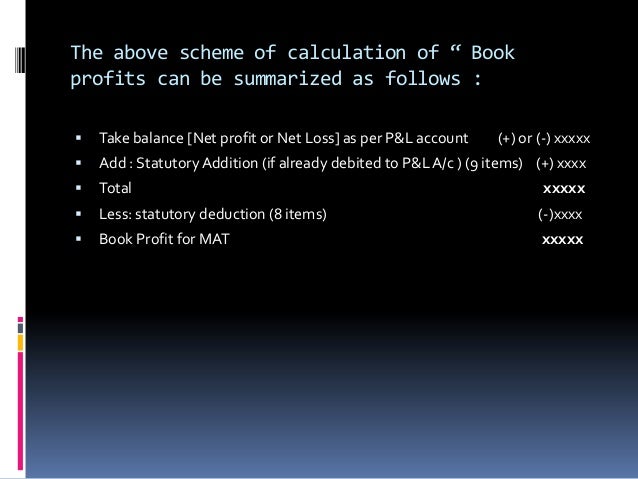

Ppt Minimum Alternate Tax Section 115jb Powerpoint Presentation Free Download Id 4406076

Calculation Of Book Profits For The Purpose Of Mat Section 115jb

Guide To Minimum Alternate Tax For Ind As Compliant Companies

Caknowledge In Minimum Alternate Tax

Mere Provision Not Eligible For Adjustment Against Book Profit It Must Be Ascertained Liability

Section 115jb Of Income Tax Act 1961 After Budget 2016

Understanding Minimum Alternate Tax Most Easy Way Youtube

Ca Final Question Bank Dt Minimum Alternate Tax Mat

Https Www2 Deloitte Com Content Dam Deloitte In Documents Tax In Tax Minimum Alternate Companies Noexp Pdf

Corporate Tax

Minimum Alternate Tax Mat Section 115jb

How To Calculate Book Profit Partnership Firm

Prometrics Finance Minimum Alternate Tax Mat Dividend Distribution Tax Ddt Applicable To Assesses Who Are Corporates

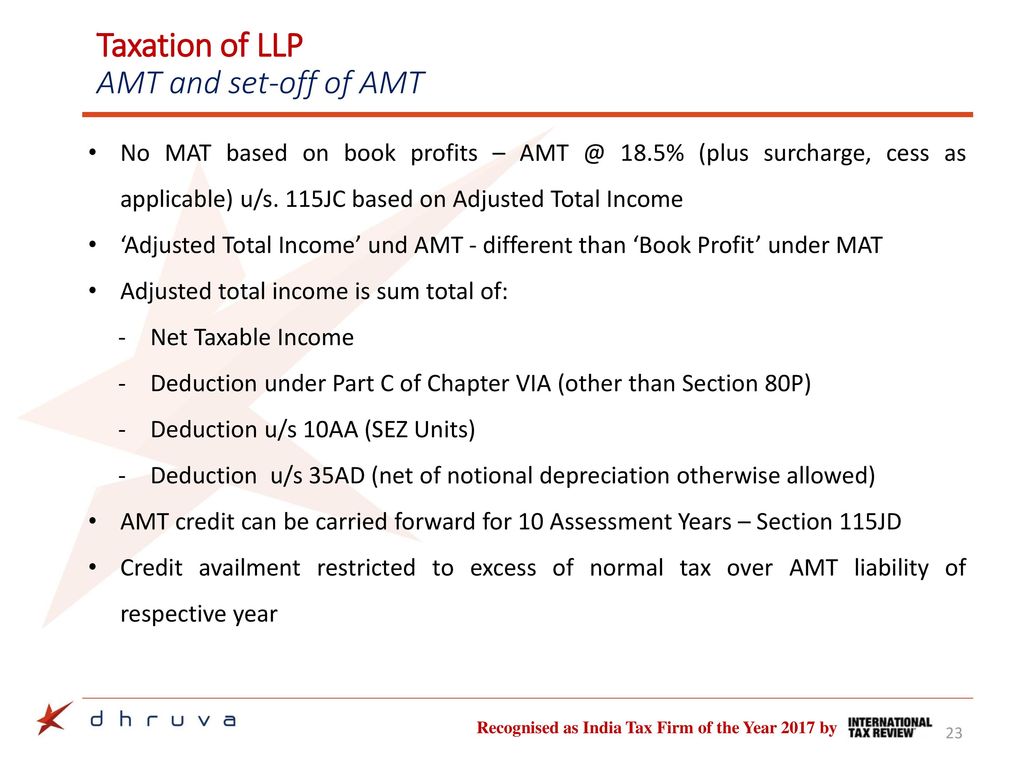

Taxation Of Llps Business Reorganisation Of Llp Ca Saurabh Shah Direct Tax Refresher Course Organized By Wirc Baroda 3 June Ppt Download

Assessement Of Companies

Analysis Of Taxation Laws Amendment Ordinance 2019 Zoho Blog

Https Icaiahmedabad Com Pdf September 17 E Newsletter Abad Wicasa Pdf

Bedtime Story Books Bedtime Story Books Stories For Kids Bedtime Stories

All About Deferred Tax And Its Entry In Books

Tax Reconciliation Under Ias 12 Example Ifrsbox Making Ifrs Easy

Transition To Ind As K Chandra Sekhar By Gm Company Secretary Ppt Download

Horizontal Format Of Balance Sheet Balance Sheet Balance Sheet Template Accounting

Https Www Pwc In Assets Pdfs Publications 2017 Pwc Reportinginbrief Mat Amendment Pdf

Source : pinterest.com